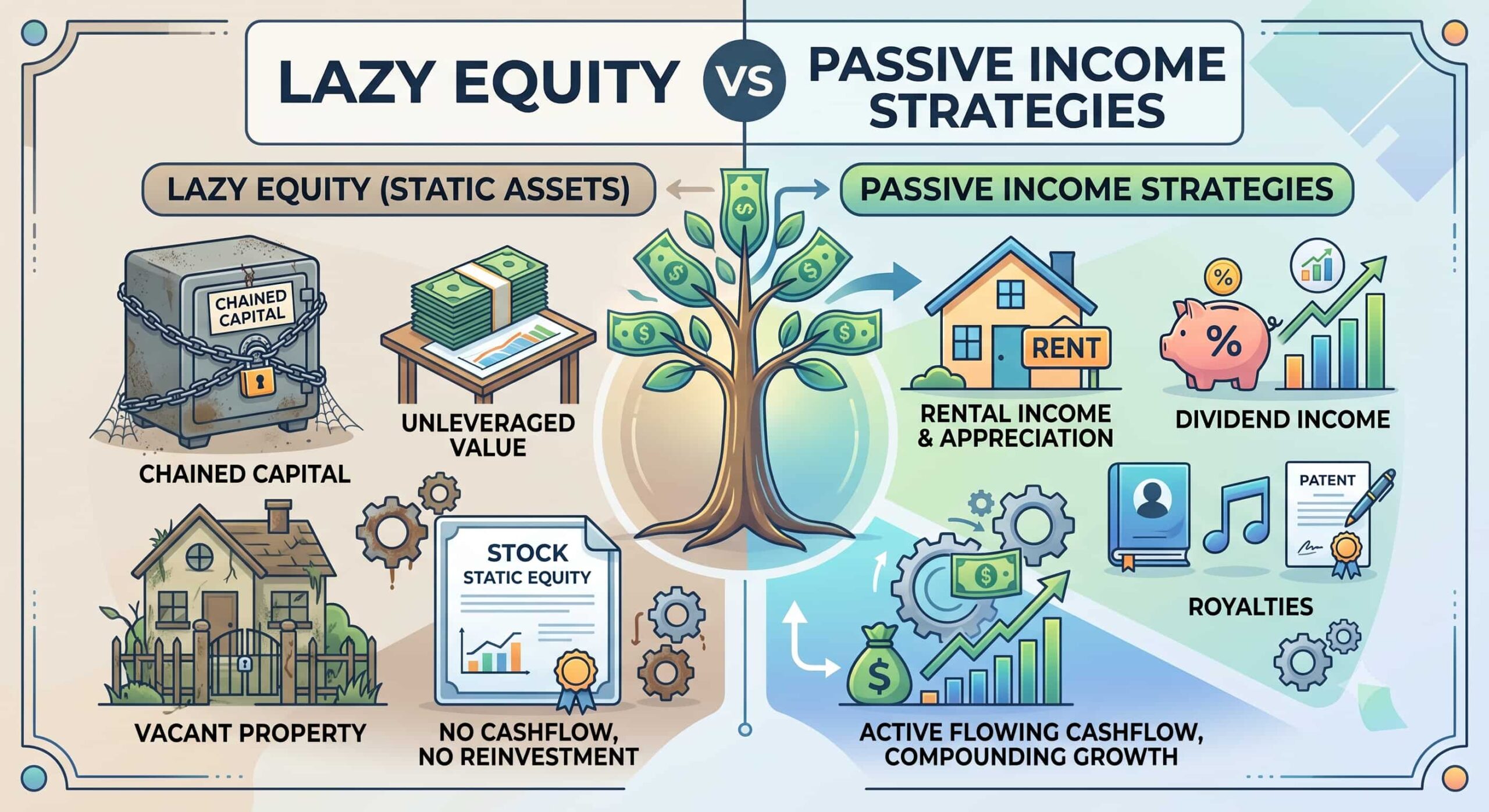

Everyone wants passive income. The dream is simple: money flowing in without active effort. But there are dozens of ways to pursue this dream, and most of them disappoint.

Passive income strategies range from dividend stocks to rental properties, peer-to-peer lending to cryptocurrency staking. They all promise wealth-building with minimal effort. In reality, most require significant work, involve substantial risk, or deliver mediocre returns.

So where does lazy equity fit? And more importantly, how does it compare to other popular passive income strategies?

This article compares lazy equity to the most common alternatives, showing you which strategies actually work and why lazy equity wins for most people. By understanding the tradeoffs, you’ll make a smarter choice about your financial future.